Some of the most common questions I receive: how does health insurance work in retirement? What insurance should I have? How much will it cost?

First, it is important to know that your options change as you age. I will go through all the various options that you have chronologically. This does not mean you will have each of these forms of health insurance – but instead, these are just your options. Analyzing the cost of your options should be done at every step. While you might be eligible for COBRA through your work – that does not mean that it is the best option.

While it seems a little daunting, you actually have plenty of options for health insurance in retirement and it presents a huge tax planning opportunity. Where you might feel fear when thinking about losing employer-subsidized insurance in your older age, I view it as a great opportunity to help you find the best balance between cost and protection.

Consolidated Omnibus Bill Reconciliation Act (COBRA)

COBRA is the name of the legislation that was passed that allows you to remain on your employer-sponsored insurance for 18 months after ending your employment. Even death allows for the widowed spouse to maintain coverage. The only stipulation is that your employer must employ more than 20 full-time individuals.

COBRA coverage requires the employer to provide you with the same group-term coverage you were in during your employment but they have no obligation to provide any employer assistance in the cost. They can actually charge you up to 102% of their standard group-term rate.

When to use this: typically, this type of coverage is great for gap coverage in high-income years. Let’s say you made $100,000 this year and end employment on Oct 1st. You still have 3 months left in the year that you need to receive coverage but you are far past any Obamacare subsidy eligibility. In that circumstance – it is likely that 102% of the group rate could be similar to your family rate on Obamacare without any assistance.

Another circumstance to use this is if you want high-quality healthcare and can afford the cost. The tradeoff with COBRA is that it is usually good coverage and thus expensive. It isn’t common that we can find a lower-cost policy on the exchange with the same benefits but it is possible to find a lower-cost policy on the exchange with lower benefits.

Obamacare

Depending on your state, you will either apply for insurance through the state’s exchange or through the federal government’s website. Obamacare allows you to purchase health insurance from private health insurance companies participating in the federal marketplace.

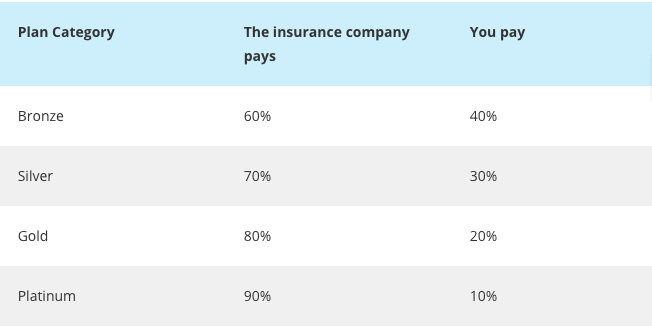

There are four types of policies: Bronze, Silver, Gold, and Platinum.

Intuitively, the cost of the health insurance plan rises in cost as the categories go from Bronze to Platinum. This means the inverse is also true: deductibles, co-pays, and overall out-of-pocket costs for plans are much higher in Bronze and Silver plans compared to Gold and Platinum. If you want a predictable (but high) monthly health care cost – the Gold and Platinum plans are built for you. If you want low (but unpredictable) monthly health care cost – Bronze and Silver are the plans to look at.

Within these tiers of plans are all types of insurance offerings. HMOs, PPOs, EPOs, and POS are all available within the exchange. In the spirit of keeping this a blog post versus a book – I will not individually explain how each one differs but each plan has a different level of doctor participation.

Obamacare premiums are dependent on your Modified Adjusted Gross Income (MAGI). The critical number to know is 400% of the poverty line. As of 2020, that number is $67,640 for a family of 2. What does this mean? You will have to pay the full stated price for your Obamacare health insurance policy if your MAGI is above that number. If you are close to or below that number – then we have a tax planning opportunity.

Keeping yourself below 400% of the poverty line is by far and large the most important thing for you to do. This is a cliff tax. If you go $1 over the limit, you could owe several thousands more in taxes (or premium subsidy repayment – to use precise vocabulary).

When to use this: It is highly likely that you will be using Obamacare at some point to provide you with health insurance in retirement if you or your partner are retiring before age 65. You could avoid Obamacare if you retire only 18 months before age 65. In that circumstance, you can utilize the COBRA coverage through work until Medicare starts. However, Obamacare is likely the best option for you if you can receive subsidy assistance by keeping your MAGI below 400% of the poverty line.

Quick note: marketplace insurance does have the option to be a high deductible healthcare plan (HDHP). You can make deductible contributions to a Health Savings Account (HSA) which reduces your MAGI if your plan meets the IRS defined requirements for HDHPs. The plan should state that it is an HSA-eligible plan pretty clearly. Generally, HDHPs are best for healthy individuals with lower annual medical costs. However, having that additional flexibility of reducing MAGI by $3,500 or $7,000 might be the difference between getting below 400% of the poverty line.

If you believe your income is going to be far above that mark – please check out my post on the Retirement Income Roller Coaster on ways to keep your income below 400% of the poverty line in *some* years of retirement.

Non-Marketplace Insurance

This is basically just private insurance bought outside the health care exchanges. These plans are not eligible for Obamacare subsidies but can be cheaper than the insurance options provided on your state’s marketplace exchanges.

Non-marketplace does not mean non-compliant health insurance. The Obamacare regulations made it so health insurance providers must provide minimum essential coverage for certain services. However, non-marketplace insurance does not mean everything is compliant either. There are especially more non-compliant plans since the Trump administration has rolled back regulations of insurance companies and made it easier to offer catastrophic-only plans. Thus, it is very important to understand your policy when buying off the exchange.

Generally, you will find these policies through using a health insurance broker. It is important that you find a competent broker that understands your needs and works in your interest. The National Association of Health Underwriters is a good place to start.

When to use this: sometimes Obamacare policies are just too expensive where you live. This can especially be the case if you are well above the 400% poverty line and you cannot find a way to reduce your income. Also – this may make sense if you are only retiring a few months before Medicare eligibility and you only need a gap plan.

Health Care Sharing Ministries

These are lesser-known and uncommon health insurance options – but they are an option. A health care sharing ministry is an organization that collects premiums and shares the collective cost of medical care amongst the members. Generally, this type of coverage is provided by religious organizations which typically has restrictions on membership based on sexuality or religion. There is also a “statement of beliefs” that must be signed to join a health care sharing ministry along with a pledge to undertake healthy behaviors.

These plans are risky. While this counts as insurance for purposes of the Obamacare shared responsibility tax penalty (which was reduced to $0 starting in 2019), this is not true health insurance. They don’t use actuaries, they are not regulated by the department of insurance, and they do not make guarantees of coverage.

When to use this: If Obamacare and COBRA coverage are both outside your price range and you would prefer to take a more collective approach to medical costs, a health care sharing ministry could be right for you.

Medicare

You hit age 65! You are officially in the golden years. Medicare is a great step up from almost every option before age 65 (besides employer-provided coverage) and it is also a requirement. If you do continue to work past age 65, you do not have to enroll in Medicare but you must let them know that you intend to stay on your employer coverage. After you end your employment, you are eligible to start Medicare. If you delay Medicare without having a reason, you may be subject to a penalty equal to 10% of the Part A premium for each month you didn’t have coverage (that’s a lot).

So what is Medicare? It is the largest health insurance provider in the United States. As long as you (or your spouse) have 40 quarters of Social Security covered employment – you are eligible for Medicare benefits. This will be stated on the Social Security Benefits report that the SSA sends you or you can access through Social Security’s website.

There are 3 medical coverages under Medicare. Part A coverage is referred to as hospital coverage. Part B coverage is for doctors. Part D coverage is for prescription drugs.

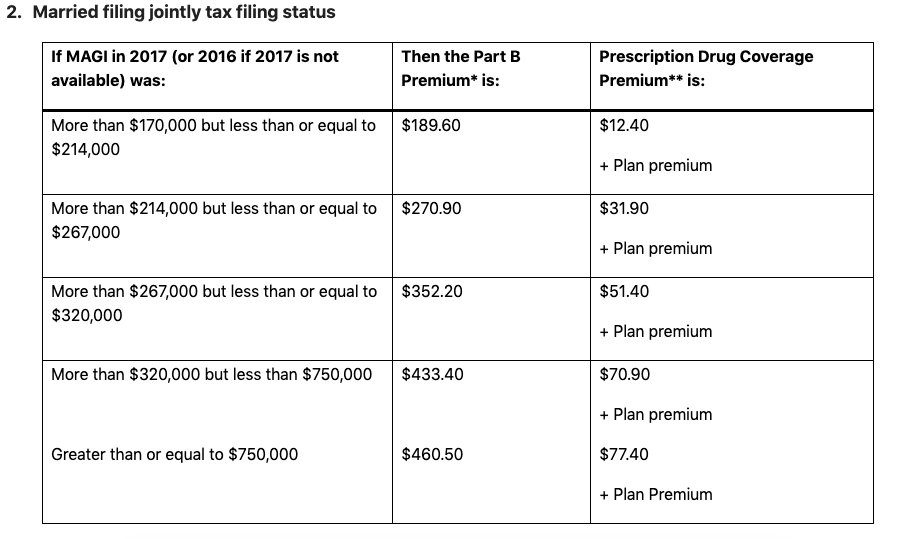

The cost of Part A is what you worked hard for all these years. You pay nothing for Part A coverage. Part B coverage does come at a very reasonable cost as long as your income remains low. The average American will pay $135.50 per month in 2019. This is 25% of the cost of the actual coverage to the government. Why do you need to know this? Because we have yet another tax opportunity – Medicare’s Income Related Monthly Adjustment Amount (IRMAA).

IRMAA is an increase in your Medicare Part B and D premiums that is based on your income. Most people won’t ever be impacted by IRMAA, but you might. Couples with MAGI above $170,000 are subject to the IRMAA tax cliffs. Let’s look at the table below (you can find the data here):

Roughly every $50,000 results in an increase in premiums (for two people – in most circumstances). Tax planning is critical if you fall within the IRMAA cliffs. You could save a few thousand dollars by actively projecting and controlling the timing of your income in between these cliffs. Don’t end the year with $171,000 in MAGI. That last $1,001 of MAGI will have cost you $1,596 in IRMAA “tax”.

When to use this: You WILL utilize Medicare as long as you retire and live until age 65. Medicare is still the best bang for your buck and is required even with the highest IRMAA charges. The biggest question will be covered in the next section – do you supplement this coverage in any way?

Quick note. If you are on a HDHP in the same year that you become eligible for Medicare, you need to be careful. You cannot put money into an HSA while you are enrolled in Medicare. This could require a withdraw of excess contributions from your HSA to avoid a penalty.

Medigap vs Medicare Advantage

These policies cover “the holes” that Medicare doesn’t cover in exchange for an additional monthly premium. Medicare does have deductibles, copays, and coinsurance. You can convert some or all of the deductibles, copays, and coinsurance into a monthly premium through these two options.

Medigap coverage comes in many letters: from A through N with a few non-conforming states. Each coverage plan fills different holes. The most common plan is Plan F: which comes in a high deductible form and a standard form. Plan F is the most comprehensive and costly Medigap policy that covers basically all of the deductibles, co-pays, and coinsurance with traditional Medicare.

Quick note. At certain ages, it turns out the Medigap high deductible Plan F may result in lower premiums that exceed the potential increase in deductible. This results in a lower cost plan in all circumstances. This may be changed in the future but annually checking the coverage for opportunities like this.

A Medicare Advantage Plan (MAP) is your next alternative. MAP is also called Part C coverage. However, the mechanics behind it are much more complicated than Medigap policies. MAPs effectively convert your Part A, B, and D Medicare coverage into private insurance that must follow Medicare rules. This is an all-in-one option versus the Medigap which is two levels of insurance. MAPs have the ability to charge different out-of-pocket costs and require different rules for services like referrals. However, MAPs can be significantly cheaper and more customizable.

When to use this: generally, it is best to use a Medigap policy or a MAP if you experience a high level of ongoing medical expenses or if you are risk-averse. Both of these plans convert coverage gaps into a monthly cost. Medigap Coverage F is the highest cost end of the spectrum with the most coverage. MAPs typically have the most custom plans and there are even MAPs that have no out-of-pocket premium but offer very few coverage benefits. It is important to look at the options and perform some cost-benefit analysis and stress testing on both types of policies given your individual medical history. I tend to lean towards Medigap policies as they are more understandable, comparable, and can reduce your medical cost risk in a clear fashion. Insurance agents tend to lean more towards MAPs.

No Health Insurance

Don’t do it. It is not worth it. You should have health insurance if you can afford it. You are exposing your whole family to risks that aren’t justified. Don’t do it.

What about Dental or Vision?

Unfortunately, you typically have to purchase dental and vision coverage separately for all these plans except through COBRA coverage, some health care sharing ministries and MAPs. Dental and vision coverage can be purchased through private insurance providers.

Recap

These are the health insurance options that you have. Your health insurance in retirement is intimately intertwined with your MAGI and income recognition. Proper income tax planning becomes so critical when basic expenses like health insurance are impacted by the income that you have to report.

Lastly, the best investment that you can make is to invest in your own health. Finding the lowest-cost, highest-benefit health insurance is wonderful but the best insurance is the insurance that you DON’T NEED TO USE. Take time to invest in your health. Adopt a dog and go on more walks. Eat healthier. Always go to your annual check-ups. Prevention is the most valuable way to spend your time and energy. But tax planning is definitely in second.