The Retirement Income Roller Coaster is a tax planning opportunity that I navigate for my clients. It is exactly as it sounds, the income that we recognize in retirement resembles a roller coaster ride. In some years we may recognize a lot of taxable income. In others, we will recognize very little. Why would we want to do that? Well, to understand that, we need to understand how tax brackets work in retirement.

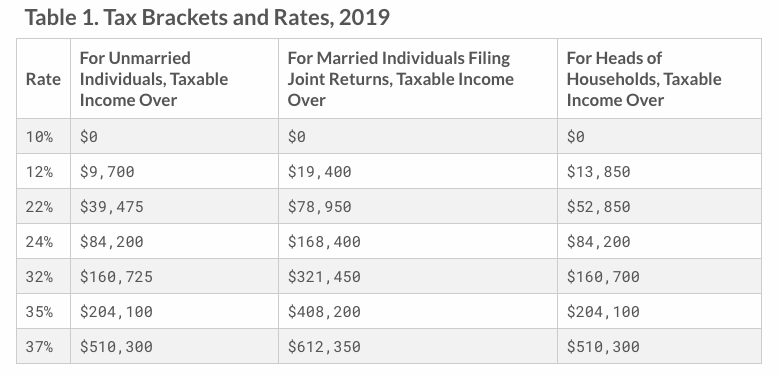

Below is the standard tax table in 2019 (with data taken from here):

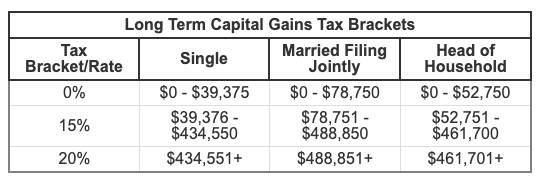

I will focus on a married couple for this article’s purposes. As you can see, it looks pretty straightforward. As your income rises, your tax bracket rises. But, of course, tax planning is never straightforward. This is strictly for ordinary income. We have another concurrent layer of capital taxation on taxable investments as seen below (with data taken from here):

Now that we know these exist, let’s add more.

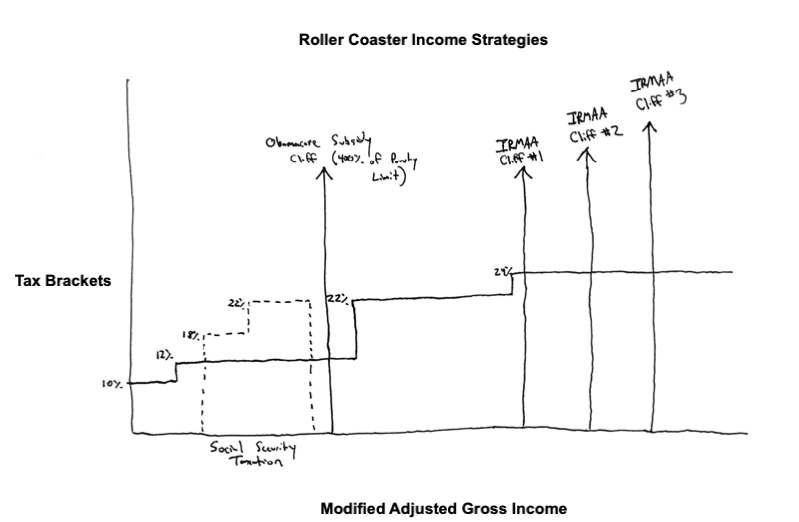

We have health insurance-based taxes that come in two forms: Obamacare Premium Tax Credits (PTC) and the Medicare Income Related Monthly Adjustment Amount (IRMAA). These additions are both cliff taxes. A cliff tax is where a single dollar of income can cause you to incur a lump sum of taxes. To avoid having too many graphics, here are the IRMAA income limits and the PTC has one cliff at 400% of the poverty line which is $65,840 in 2019.

Social Security is also taxed in an obscure way. Social Security is not taxed if your income is below a certain threshold. Once your income exceeds that threshold, either .50 cents or .85 cents of Social Security benefits start becoming taxed with each additional dollar of income. This effectively doubles your tax bracket for this range of income. Once all of Social Security is subject to taxation, the tax bracket actually falls back down to the normal ordinary bracket shown in this first graphic.

Here is a literal hand-written version of what I talked about.

I avoided using actual dollar amounts on purpose. The dollars are not the same for everyone especially considering different filing statuses and Social Security benefits. Every dotted line and spike is a potential opportunity (or cost). When tax brackets go up and then back down, that is another opportunity.

Single individuals even have the off chance of having a 40% marginal tax bracket for a small portion of their Social Security taxation. This only happens when they have a really high Social Security benefit (>$30,000 of annual benefits)

This is why tax planning is so critical. Every additional layer of tax code complication creates the opportunity to save massive amounts of taxes by proactively planning when you recognize income.

Now let’s discuss the roller coaster strategy. How does the roller coaster strategy benefit you? Well, it directly relates to the cliff taxes and Social Security taxation. It is not reasonable to assume that we can keep your taxes low every year of retirement – but why can’t we structure your income in a way where we can take advantage of the PTC or Social Security bracket jump in MOST years?

Let’s look at an example.

Jack and Jill are 62 years old and have been retired for about 7 years. They accumulated all of their assets in pre-tax 401(k) accounts while working and they pull around $60,000 from them on an annual basis to cover their living expenses. Since Jill was the breadwinner and Jack has been in poor health, they decided to start Jack’s SS benefit at age 62. This results in $12,000 per year of additional dollars which they will use to take a 3 month-long trip to a new country.

Since Jack and Jill are not at Medicare age yet, they have their health insurance through Obamacare. They both spend around $700/mo. on Silver plan coverage and they receive around $800/mo. in advanced premium tax subsidies. However, now that Jack is taking Social Security every year – they are no longer eligible for the $800/mo advanced premium tax subsidy.

Since 85% of the Social Security benefits are included in their Modified Adjusted Gross Income (MAGI), the total MAGI for Jack and Jill is $70,200. This is $4,360 away from 400% of the poverty line and causes them to pay full boat for their health insurance. By reducing their income by $4,360, it is very likely that they will save over $10,000 in health insurance premiums. But how do we accomplish that?

They have two options:

- Stop Social Security and repay it within 12 months + not go on the trip

- Income Roller Coaster

Do you want to be the one to tell Jack that he can’t go on the 3-month long international vacation that he has worked all his life for? Me neither. Especially not when the Income Roller Coaster will achieve the objectives and let him continue to live the life he wants to live.

The mechanics behind the Income Roller Coaster are simple: let’s add enough income this year so that all future years until Age 65 can have income below 400% of the poverty line:

Since they are squeezing just under 400% of the poverty line (assuming that it goes up slightly each year for inflation) they are only responsible to pay approximately 10% of their income as health insurance premiums. That is HUGE. By simply recognizing $22,000 of additional taxable income at age 62 at a tax rate of 12%, we are able to save $35,000 of tax + health insurance premiums in the next two years.

Now, while this is a practical example, I did cherry-pick this situation. It is not too often that someone is that close to the cliff tax. However, this strategy can be beneficial at much greater income differentials. Let’s say they need to spend an additional $20,000 to live their best life.

We still manage to save $27,000 of tax + health insurance premiums given a scenario that might align better with a realistic version of your life. This does require an upfront tax payment of $16,060 more than what we would have normally paid in that year. However, that is purely the investment needed to efficiently manage your taxable income for the next two years.

The Income Roller Coaster strategy can apply to IRMAA as well. It can apply to Social Security taxation. It can be used while you have Required Minimum Distributions. It can be used if you are subject to the Net Investment Income Tax. All taxes that are imposed at different levels of income and especially all cliff taxes can be minimized with this approach. This doesn’t mean that you will never pay a cliff tax – but you can absolutely structure it to where you are only paying the cliff tax every few years. The tax savings are incredible.

Recap

This is always the recap for any tax-related post but you NEED to be properly planning your income recognition in retirement. While I view this as an opportunity, the converse is that messing this up is a huge mistake. Going over a cliff tax when you didn’t need to can cost you so much money. Make your financial independence more secure by controlling something that is actually controllable – your tax planning.